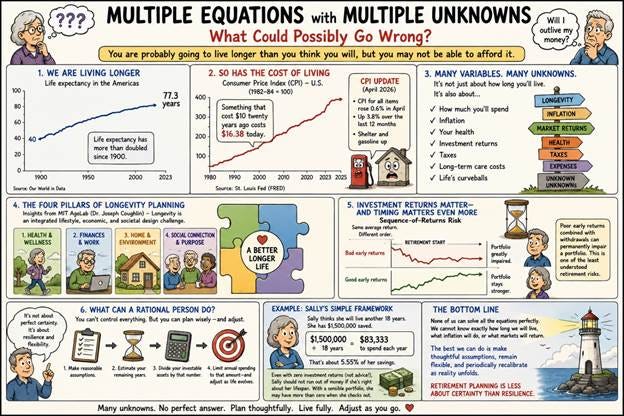

Multiple Equations with Multiple Unknowns

What could possibly go wrong?

Good news and bad news: you are probably going to live longer than you think you will, but you may not be able to afford it.

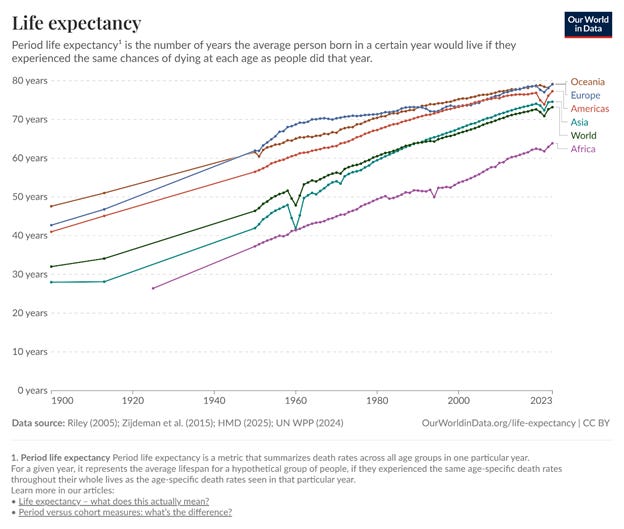

Life expectancy has soared since the 1900s. This chart from Our World in Data[1] shows life spans from around the world and how they have changed over time. In the Americas, for example, life expectancy has risen from just over 40 years in 1900 to 77.3 years in 2023.

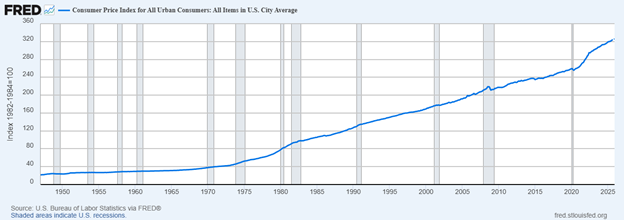

Unfortunately, the cost of living has gone up a lot, too. Check out this Consumer Price Index chart from the St. Louis Fed’s FRED data base[2]:

That’s an ugly picture! To put it into perspective, something that cost $10 twenty years ago, would cost $16.38 today, according to the US Inflation Calculator.[3]

Adding more ugliness to the picture was this morning’s Consumer Price Index (CPI) news release from the U.S. Bureau of Labor Statistics[4]:

CPI for all items rises 0.6% in April; shelter and gasoline up

05/12/2026

In April, the Consumer Price Index for All Urban Consumers rose 0.6 percent, seasonally adjusted, and rose 3.8 percent over the last 12 months, not seasonally adjusted. The index for all items less food and energy increased 0.4 percent in April (SA); up 2.8 percent over the year (NSA).

Figuring out if you are going to outlive your money is no easy task. It’s not only about how long you’re going to live, but it’s also about how much you’re going to spend. How much you’re going to spend depends on things like inflation and how healthy you’ll be.

If you are curious about how long the Social Security Administration thinks you’ll live, check out their calculator at Retirement & Survivors Benefits: Life Expectancy Calculator. Your results may vary!

And if you’d like to know what might be responsible for variations from SSA forecasts, check out the work at the MIT AgeLab[5] (hat tip to friend and former colleague, Justin Bardin). Dr. Joseph Coughlin, leader of the AgeLab, has as his broad thesis that longevity is not just a medical issue – it is an integrated lifestyle, economic, and societal design challenge.

He has described four major “longevity planning blocks” or “domains” as follows:

1. Health & Wellness

2. Finances & Work

3. Home & Environment

4. Social Connection & Purpose

Here’s an unsettling thought: what if Peter Diamandis[6] is right and “science can extend life faster than ageing progresses…and we achieve a form of biological immortality”? I can guarantee you the even highly professional Certified Financial Planners are not planning for life beyond 150 years!

And notice something important: I have barely mentioned investment returns. It’s not because they aren’t the most important input (they are not), it’s because not only are the absolute returns important, it’s because the order they come in are critically important, too. Financial planners refer to this as “Sequence-of-Returns Risk:

A critically important concept.

Two retirees can earn:

· the exact same average return,

· but have radically different outcomes depending on WHEN losses occur.

Poor early retirement returns:

· combined with withdrawals,

· can permanently impair a portfolio.

This is one of the least understood retirement risks.

Will I outlive my money? Good luck trying to figure it out! You can control your spending, but not the prices of the goods and services you buy. You cannot control (or forecast with any certainty) the return on your investments.

In light of the difficulty associated with answering this question, what’s a rational person to do to avoid freaking out?

Make some reasonable assumptions, then adjust as time passes. Get an estimate of your potential remaining years on planet Earth. Divide your investable assets by that number then limit your annual spending by that amount. Here is an example:

Based on the SSA data, Sally thinks that she will live another 18 years. She has saved $1,500,000 in various qualified and non-qualified accounts.

$1,500,000 / 18 = $83,333 to spend each year or approximately 5.55% of her retirement savings. Please do not take this as a recommendation or investment advice, but I think this number compares favorably to the old 4% rule of thumb.

This does not consider taxes or inflation. But what it says is that even if Sally put her money under her mattress (not investment advice!) and she was right about her death date, she would not run out of money. If her investment advisor is able to structure a portfolio of stocks, bonds, gold and cash that returns more than the mattress, she will have more than zero when she checks out.

In the final analysis, not outliving your money is a very big deal indeed. But I’ve come to the conclusion that Alan Jackson and Dr. Joe from AgeLab are correct, “the older I get, the truer it is; It’s the people you love, not the money and stuff, that makes you rich.”

[2] Consumer Price Index for All Urban Consumers: All Items Less Food and Energy in U.S. City Average (CPILFESL) | FRED | St. Louis Fed

[3] Inflation Calculator | Find US Dollar’s Value From 1913-2026

[4] https://www.bls.gov/cpi/news.htm

[5] Joseph F. Coughlin | MIT AgeLab

[6] CAN WE LIVE FOREVER? Peter Diamandis On AI, Aging & Longevity Escape Velocity